The Unified Fixed Income Trading Platform: A New Operating Model for Modern Wealth Firms

Modernizing Fixed Income Operations for RIAs, IBDs, TAMPs, and Asset Managers

Fixed Income Has Become a Technology Problem

Over the last two decades, wealth firms have industrialized the way they trade equities. Orders that once moved by phone now route through systems. Allocations that once lived in spreadsheets now resolve automatically. Rebalancing, models, oversight, and reporting became repeatable enough for firms to scale without adding a person for every new account.

Fixed income never got that treatment.

Almost everything that makes equities easy to systematize is absent in fixed income. There is no central exchange; pricing is not continuous or fully transparent. Liquidity is scattered across dealers and venues. A single issuer can have dozens of outstanding securities, and the broader market spans millions of individual CUSIPs that may trade infrequently.

As a result, many firms still manage fixed income through workflows built around dealer relationships, spreadsheets, disconnected systems, and advisor-specific processes, which often work well at a smaller scale. As allocations increase, however, the amount of operational coordination required to maintain them grows rapidly.

At Flyer, we see the same pattern repeatedly across RIAs, IBDs, TAMPs, and asset managers. Fixed income becomes increasingly important to client portfolios, but the systems supporting it remain separate from the rest of the firm’s operating model.

The challenge is rarely access to bonds, but coordinating execution, portfolio management, compliance, allocation, reporting, and ongoing maintenance across growing numbers of accounts.

Many firms approach fixed income as a trading problem.

In practice, fixed income is an operating model problem.

Trading is only one component. Every position must move through portfolio construction, compliance oversight, allocation, settlement, reporting, maturity management, and reinvestment workflows. As fixed income allocations grow, the ability to coordinate those activities becomes increasingly important.

The firms that scale fixed income most effectively do not simply improve execution. They build infrastructure that connects execution, portfolio management, and workflow management into a single operating environment.

This guide explores how modern firms approach fixed income trading, portfolio management, and workflow design, and how those functions can operate inside a single environment rather than across disconnected tools.

What Is a Fixed Income Trading Platform?

Your UMA isn’t unified. It’s stitched together.

A fixed income trading platform is software that helps wealth management firms source bond inventory, request dealer quotes, execute trades, allocate positions, manage compliance, and oversee fixed income portfolios from a centralized environment.

Some fixed income platforms focus primarily on market access and execution, while others support the broader operating model of the firm by connecting execution, portfolio management, compliance, allocation, reporting, and oversight.

The distinction becomes increasingly important as firms grow.

Fixed income workflows do not end when a trade is executed. Positions must be allocated, monitored, reconciled, reported, rebalanced, and maintained throughout their lifecycle. A platform that supports only execution still leaves much of the operational burden untouched.

The most effective fixed income trading platforms support the full lifecycle of a bond position rather than a single point within it.

What Is a Bond Trading Platform?

A bond trading platform is technology used to source bond inventory, compare pricing, request dealer quotes, and execute fixed income transactions.

While the term is often used interchangeably with fixed income trading platforms, bond trading platforms vary significantly in scope. Some focus exclusively on trade execution and market access. Others support broader functions such as portfolio management, allocation, compliance oversight, reporting, and workflow management.

For wealth management firms, the differences become increasingly important as fixed income allocations grow. Execution is only one step in the process. Positions must also be allocated, monitored, reported, rebalanced, and managed throughout their lifecycle.

As a result, many firms are moving beyond standalone bond trading tools and toward platforms that connect execution with the broader operating model of the business.

Why Fixed Income Breaks the Equity Playbook

To understand why fixed income becomes difficult to scale, it helps to understand how the market itself is structured.

Equities trade on centralized exchanges with continuous pricing and visible liquidity, but fixed income operates differently.

Most bonds trade over the counter across a fragmented landscape of dealers, counterparties, custodians, and venues. The same security may be available from multiple dealers at different prices depending on inventory, timing, and market conditions.

Liquidity is often relationship-driven rather than exchange-driven.

Why Fixed Income Is Harder to Scale Than Equities

- Centralized Exchange

- Continuous Pricing

- Transparent Liquidity

- Standardized Workflows

- Automated Execution

- High Trading Frequency

- Centralized Exchange

- RFQ Pricing

- Variable Liquidity

- Complex Workflows

- Relationship-Driven Execution

- Often Infrequent Trading

Why Liquidity Is Fragmented in Fixed Income Markets

Unlike equities, bonds do not trade through a single centralized marketplace.

Individual securities often trade infrequently, dealer inventories constantly change, and pricing varies across counterparties. Two firms looking at the same bond at the same time may receive different quotes depending on the dealers they can access.

Fragmentation is one of the defining characteristics of fixed income markets, a primary reason fixed income workflows have historically relied on phone calls, dealer relationships, and manual execution processes.

What RFQ Trading Is and How It Works in Fixed Income

Because there is no centralized order book, fixed income execution typically follows a Request-for-Quote (RFQ) model.

Rather than executing against a displayed market price, traders request quotes from multiple dealers, compare available responses, and execute against the preferred quote.

RFQ workflows create competition among liquidity providers and support best execution practices. They also introduce workflow complexity that equity-oriented systems were never designed to manage.

These structural elements influence everything that follows, from execution and compliance to allocation, rebalancing, reporting, and oversight.

How Modern Firms Organize Fixed Income Operations

Firms that scale fixed income successfully typically organize the process across three connected functions:

Execution

Liquidity access, dealer connectivity, RFQ workflows, and trade execution.

Portfolio Management

Portfolio construction, duration management, bond ladders, risk oversight, and rebalancing.

Workflow Management

Compliance, allocation, settlement, reconciliation, reporting, and operational controls.

These functions typically sit across different teams, but they work best when connected through a coordinated operating model rather than separate tools and manual handoffs.

This is the infrastructure layer that many firms discover they are missing.

Fixed income may appear to be a collection of trades, but operationally it behaves like a system. Execution affects allocation. Allocation affects reporting. Reporting affects oversight. Compliance touches every stage of the workflow.

When those functions operate independently, complexity increases. When they operate as a coordinated system, firms gain greater consistency, visibility, and scalability across the organization.

Fixed Income Is Infrastructure

The conversation around fixed income technology often begins with trading.

In reality, execution is only one layer of the process. Portfolio construction, compliance, allocation, reporting, maturity management, and post-trade operations all influence the effectiveness of a fixed income program.

As firms grow, fixed income increasingly behaves like infrastructure rather than a standalone investment activity.

The organizations that scale most effectively tend to build coordinated frameworks that connect execution, portfolio management, and operational workflows into a single system.

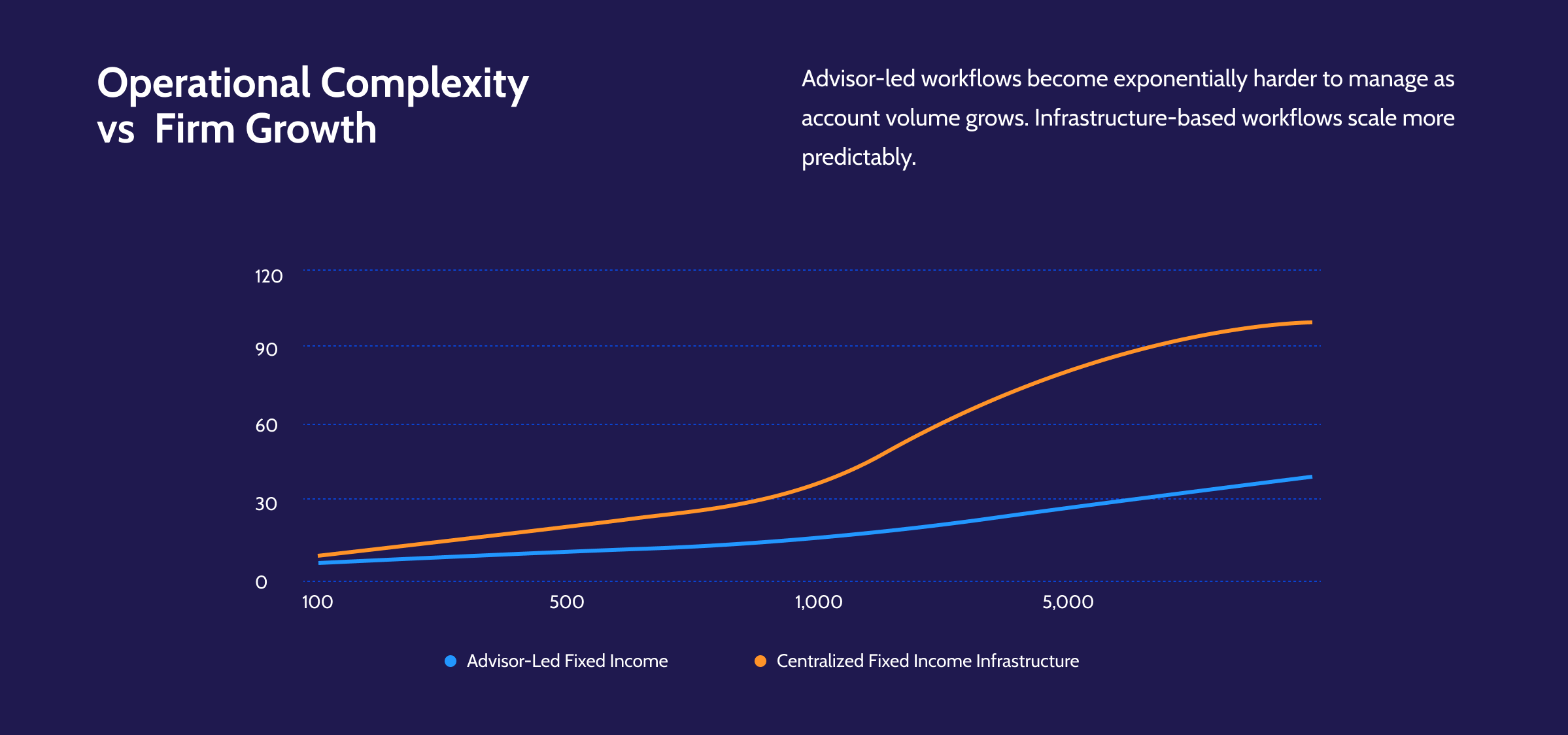

Where Advisor-Led Fixed Income Stops Scaling

At many firms, fixed income remains advisor-led.

The advisor identifies the bond, evaluates pricing, executes the trade, allocates the position, tracks maturities, and manages reinvestment decisions. The entire process lives inside one person’s workflow.

- Volume increases.

- Advisors develop slightly different execution processes.

- Pricing visibility becomes inconsistent.

- Compliance reviews occur after the fact because no structured checkpoint exists within the workflow.

- Maturity management depends on individual follow-through rather than systematic oversight.

As a result, firms experience increasing operational complexity.

Bonds require more coordination, monitoring, and operational effort per dollar of AUM than many other asset classes. As firms expand, the conversation often shifts from security selection to process design.

Many firms initially respond by adding another bond system, which creates yet another layer of complexity rather than removing it. The way forward is a shift in the operating model that connects execution, portfolio management, and workflow management through a coordinated infrastructure.

Related Resources

Fixed Income as an Operating System

Scaling effectively requires managing fixed income as a coordinated process rather than treating each bond trade as an isolated event.

Execution, portfolio management, compliance, allocation, reporting, and oversight remain distinct functions, but they operate within the same workflow instead of across disconnected tools and manual processes.

The approach also creates a clearer delineation of roles and responsibilities:

- Trading desks manage execution and liquidity access.

- Operations teams oversee allocation, settlement, and reporting.

- Compliance becomes part of the workflow rather than an activity performed after execution.

- Advisors focus on portfolio decisions and client outcomes.

The objective is not to remove advisors from the process but to reallocate operational work that does not require advisor judgment so advisors can focus on portfolio decisions and client relationships.

The Execution Layer

The execution layer determines how firms access liquidity, compare pricing, document best execution, and move trades into downstream workflows.

What Is the Difference Between an OMS and EMS

An Execution Management System (EMS) focuses on liquidity access and execution quality. Traders use EMS technology to aggregate dealer quotes, manage RFQ workflows, compare pricing, and document execution decisions.

An Order Management System (OMS) manages the lifecycle of an order, including creation, routing, allocation, and recordkeeping.

Many firms experience operational friction when execution and order management occur in separate environments. Unified OEMS infrastructure helps reduce that friction by connecting execution activity directly to allocation, compliance, and reporting workflows.

Liquidity Access and Connectivity

Connectivity determines how effectively firms can reach dealers, venues, custodians, and liquidity providers.

A firm connected to only a handful of dealers sees only a portion of available inventory and pricing; broader connectivity improves visibility and supports more consistent execution outcomes.

Trading APIs and standardized connectivity frameworks allow execution workflows to integrate directly with portfolio management, compliance, and reporting systems rather than requiring manual re-entry.

What Is a Trading API?

A trading API is a programmatic interface that allows systems to exchange trading, execution, portfolio, and market data automatically.

In fixed income operations, APIs can connect:

- Trading systems

- Portfolio management systems

- Compliance platforms

- Custodians

- Dealer networks

- Reporting environments

These integrations reduce manual work, improve data consistency, and allow firms to modernize workflows without replacing their entire technology stack.

The Portfolio Layer

Portfolio management determines what belongs in the portfolio, how risk is managed, and how allocations evolve over time.

What Fixed Income Portfolio Management Software Does

Fixed income portfolio management software helps firms construct, monitor, and adjust bond portfolios across clients, accounts, and households.

Capabilities often include:

- Duration management

- Credit exposure monitoring

- Yield analysis

- Bond ladder management

- Rebalancing

- Risk monitoring

- Household-level oversight

The objective is to help firms manage fixed income consistently while reducing manual processes and operational complexity.

What Investment Portfolio Management Software Does

Investment portfolio management software extends these capabilities across asset classes.

Rather than managing bonds, equities, options, and funds in separate systems, firms can oversee portfolio construction, risk management, allocation, and reporting from a unified environment.

This becomes increasingly valuable as firms attempt to scale fixed income alongside the rest of the portfolio.

How Fixed Income Portfolios Are Constructed

Fixed income portfolios are typically built around objectives such as:

- Income generation

- Duration targets

- Credit quality requirements

- Tax considerations

- Liquidity needs

- Maturity schedules

Portfolio managers evaluate available securities and structure portfolios to align with those objectives while balancing risk, diversification, and yield opportunities.

Many firms use bond ladders, models, sleeves, and household-level portfolio structures to improve consistency and scalability.

Managing Risk and Rebalancing at Scale

Risk management requires ongoing oversight of duration, credit exposure, concentration, and sector allocations.

Rebalancing keeps portfolios aligned with those objectives as markets and holdings evolve.

Modern portfolio management systems allow firms to monitor exposures across large numbers of accounts and implement changes systematically rather than manually.

The Workflow Layer

Execution is only one part of the process. Every trade moves through a broader workflow that includes compliance review, allocation, settlement, reconciliation, reporting, and audit management.

What the Fixed Income Trading Workflow Looks Like End-to-End

A complete fixed income workflow typically includes:

In manual environments, each handoff introduces opportunities for delay, duplication, or error.

In coordinated environments, information moves through the process with the trade itself.

Portfolio Decision

Liquidity Sourcing

RFQ

Compliance Review

Trade Execution

Allocation

Settlement

Reconciliation

Reporting

Execution is only one step in a much broader workflow.

What Is the Trade Lifecycle in Fixed Income Trading?

The trade lifecycle is the complete sequence of activities associated with a trade, from creation through execution, allocation, settlement, and reporting.

Viewing these activities as one connected process rather than separate events is essential for operational scale.

What Is Trade Processing?

Trade processing refers to the operational steps that move a trade from execution to completion.

These activities include:

- Allocation

- Confirmation

- Settlement

- Reconciliation

- Audit management

The more manual these activities become, the greater the operational burden placed on the firm.

What Is Straight-Through Processing?

Straight-through processing (STP) occurs when a trade moves through execution, allocation, settlement, and reporting without manual re-entry.

STP reduces operational risk, improves efficiency, and creates more scalable workflows.

For fixed income operations, straight-through processing is often one of the clearest indicators of operational maturity.

Fixed Income Workflows That Expose Operational Gaps

The operating-model gap becomes most visible in everyday workflows.

Bond Ladder Management

- Ladder construction

- Maturity tracking

- Reinvestment management

- Household deployment

Rolling Maturity Management

- Monitor upcoming maturities

- Generate cash events

- Trigger reinvestment workflows

Cash-to-Bond Transitions

- Identify idle cash

- Evaluate available opportunities

- Execute transitions efficiently

Household-Level Allocation

- Taxable accounts

- IRA accounts

- Joint accounts

- Trust accounts

Pre-Trade Compliance and Best Execution

- Regulatory checks

- Firm policy checks

- Best execution review

- Dealer quote comparison

- Audit-ready documentation

How Flyer Runs Fixed Income

Flyer was built around the belief that fixed income is fundamentally an infrastructure challenge, not simply an execution challenge.

Execution quality matters, but so do portfolio construction, compliance oversight, allocation workflows, reporting processes, and integration across custodians and systems.

As firms grow, those functions become increasingly interconnected. Managing them across separate systems often creates operational friction, fragmented visibility, and unnecessary complexity.

That is why Flyer was designed as a unified operating environment rather than a standalone bond trading tool.

Flyer Trading Network

The Flyer Trading Network connects firms to dealers, brokers, custodians, and venues through standardized execution workflows and connectivity infrastructure.

Co-Pilot

Co-Pilot centralizes portfolio management, rebalancing, compliance oversight, allocation management, and execution workflows within the same environment.

Open API Architecture

Because Flyer is built on an open API architecture, firms can integrate fixed income operations with existing systems rather than replacing their broader technology stack.

Multi-Custodial Operations

For firms operating across multiple custodians, the platform provides a consistent operating environment regardless of where assets are held.

Household-Level Allocation

Fixed income, equities, options, mutual funds, and cash management operate within the same workflow, giving firms one source of truth across portfolio management, execution, compliance, and reporting.

Why Firms Choose Unified Fixed Income Infrastructure

Many fixed income solutions address a single part of the workflow. Some focus on execution. Others focus on portfolio management. Others address reporting, compliance, or operational processing.

As firms grow, managing those functions across multiple systems often creates fragmented workflows, inconsistent data, and additional operational overhead.

Flyer takes a different approach by connecting execution, portfolio management, compliance, allocation, reporting, and workflow management within the same operating environment.

The result is greater visibility across the trade lifecycle, more consistent operational processes, and a technology foundation that can support growth without requiring firms to continually add systems and manual workarounds.

For organizations operating across multiple custodians, asset classes, and advisor teams, a unified infrastructure approach can simplify operations while improving consistency across the business.

Related Solutions

Building a Fixed Income Operation That Scales

Fixed income has returned as a meaningful allocation for many wealth firms.

The firms that succeed with fixed income will not necessarily be those with access to the most bonds. They will be the firms whose operating models allow fixed income to move with the same consistency, visibility, and efficiency as the rest of the portfolio.

They will be the firms whose operating models allow fixed income to move with the same consistency, visibility, and efficiency as the rest of the portfolio.

Understanding where advisor-led fixed income works—and where it begins to break down—is the first step.

Bringing fixed income into the same operating environment as portfolio management, execution, compliance, and reporting is the next.

See Fixed Income Run Inside One Platform

Request a demo of Flyer to see fixed income, equities, options, mutual funds, and cash management managed through a unified workflow.

Frequently Asked Questions

What is a centralized trading desk?

A centralized trading desk is an operating model where a dedicated team and shared system manage trade execution across all advisor accounts.

It handles execution, allocation, and oversight on behalf of advisors rather than each advisor trading independently. The model unifies order management, routing, allocation, controls, and post-trade workflows into one coordinated trade lifecycle.

What is advisor trading?

Advisor trading is the process of translating portfolio decisions into executable instructions across client accounts.

It represents the advisor-driven side of portfolio updates (intent, strategy, and client context) and how that intent becomes orders. At scale, it requires structured workflows to avoid manual handoffs and rekeying.

What is portfolio execution infrastructure?

Portfolio execution infrastructure is the system layer that connects advisor decisions directly to centralized execution workflows.

It closes the gap between portfolio intent and trade execution, allowing firms to scale AUM without increasing operational complexity.

When does Rep-as-PM and centralized trading at a Broker Dealer make sense?

Centralized trading becomes necessary when advisor-led execution no longer scales with firm growth.

Rep-as-PM works at smaller scale, where advisors manage both decisions and execution. Centralized trading becomes the right model once trade volume, account count, or model complexity overwhelm advisor-by-advisor execution—typically as firms cross $1B–$5B in AUM or have higher advisor adoption of custom or centralized model-driven strategies.

How is centralized trading different from outsourced trading?

Centralized trading keeps execution in-house, while outsourced trading delegates execution to a third party.

Both models solve the problem of decentralized trading not scaling, but trade off control versus operational lift. Centralized models prioritize visibility and control; outsourced models prioritize simplicity.

Why do RIAs centralize trading as they scale?

RIAs centralize trading to break the linear relationship between AUM growth and operational headcount.

Decentralized advisor trading creates operational drag—each new advisor introduces workflow variation, allocation errors increase, and trading teams grow just to keep up. Centralization replaces that model with scalable infrastructure.

What software supports centralized trading?

A centralized trading desk relies on an integrated system stack that shares execution context across the trade lifecycle.

Solutions typically include:

- OMS or OEMS for order and execution management

- FIX connectivity for broker and venue routing

- Embedded allocation logic

- Compliance controls

- Post-trade workflows for reconciliation and settlement

To support centralized trading, the layers need to operate as one coordinated system rather than as disconnected tools.

What does a centralized trading workflow look like step by step?

A centralized trading workflow moves from advisor intent to execution without manual translation:

Advisor submits structured intent →

System aggregates accounts →

Trading desk receives execution-ready orders →

Orders route via FIX with compliance checks →

Executions update in real time →

Post-trade workflows handle reconciliation →

Advisor sees status and exceptions in a shared view.

Why does centralized trading still feel manual at many firms?

Because the advisor-to-trader handoff is still unstructured.

Even when firms adopt modern systems, workflows often rely on emails and spreadsheets and trading teams still recreate intent manually, so operational drag persists despite better tools.

How do model portfolios create operational bottlenecks?

Model portfolios scale strategy, but they also amplify execution complexity.

Each model change affects many accounts simultaneously. Without structured execution infrastructure, that creates manual workload, exceptions, and inconsistent implementation across portfolios.

What’s the difference between OMS and EMS?

FIX connectivity enables consistent, scalable routing between trading systems and counterparties.

When implemented as engineered infrastructure, it standardizes connectivity, improves monitoring, and allows execution to scale reliably across brokers and custodians.

Why is FIX connectivity central to centralized trading?

Broker-neutral means execution is not tied to a single broker or venue.

It allows firms to maintain routing flexibility while applying consistent execution logic and connectivity standards across counterparties.

When should a firm consider re-architecting for centralized trading?

When incremental fixes stop reducing operational friction and scaling becomes inefficient.

Typical signals include rising trade volume, onboarding delays, audit complexity, allocation errors, and increasing cost per AUM dollar.

What teams typically own the decision to centralize trading?

Centralization decisions are typically led by Heads of Trading, Portfolio Management, and Operations.

CIOs and COOs are often involved when the decision intersects with infrastructure strategy and firm-wide growth planning.

Does centralization reduce advisor control?

No. Centralization separates decision-making from execution rather than removing control.

Advisors retain portfolio strategy, client relationships, and final decision authority. They offload execution mechanics, allocation logic, and operational follow-ups.

How does centralized trading improve client outcomes?

Centralized trading improves client outcomes by ensuring faster, more consistent execution across accounts.

It reduces errors, improves timing, and ensures portfolios are implemented as intended.

What happens if a firm doesn’t centralize trading?

Firms that don’t centralize trading often hit a scalability ceiling.

Operational costs rise with AUM, execution errors increase, and growth slows due to workflow constraints.